Daily Market Brief

Welcome to our first internal market brief! I’m really excited to kick this off. I’m a big believer that having a shared "pulse" on the market helps us react faster and more cohesively as a team, especially with the volatility we've seen this week.

This first memo covers the standout shifts from May 5 and 6, focusing on the diverging reads between gold, bonds, and the latest from the WGC.

The Game Plan:

The Monday Jumpstart: Starting next week, I’ll have a debrief by 7:00 AM every Monday. It’ll cover Sunday night’s overnight moves and any weekend headlines so you can hit the ground running.

Built for You: I want this to be a tool, not just a document. If there’s a specific asset class, a "weird" data point, or a region you’re watching closely, let me know. I’m happy to tailor the sections to make your lives easier.

Commodities

Oil: WTI, Brent, WCS

WTI settled May 6 at roughly $95 after dropping about 7% from Tuesday's $102 print. The fade tracks reports that Iran is reviewing a US-backed proposal to end the war via Pakistani mediators, with President Trump cautioning that Iran's acceptance is a big assumption. Brent followed it down, settling near $103, also off about 6% on the session.

WCS: Differential narrowed to WTI minus $16.00/bbl on May 5 (June delivery, Hardisty) from minus $16.25 on May 4, even as flat-price WTI dropped sharply on Iran de-escalation hopes.

The $16 print is materially wider than the post-TMX equilibrium of around $11. Two pressures stacked: SPR releases through April-May competing with WCS into PADD III, plus a global heavy-sour scarcity premium that pulled medium-sour off the market during the war. Post-deal, if Hormuz reopens cleanly, medium-sour comes back and WCS gets squeezed unless TMX volumes find Asian homes. If the deal stalls, WCS becomes one of the few reliably available heavy barrels into the Gulf Coast. Asymmetric either way.

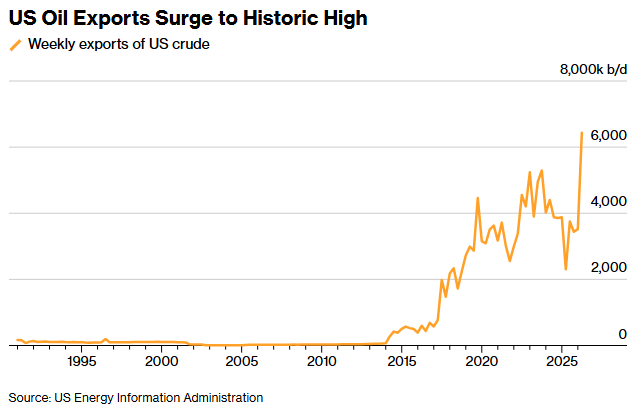

US exports are the swing barrel. Last week US crude exports hit a record as buyers redirected away from Gulf supply. That is the structural takeaway from this conflict for the next decade, not the price print.

Natural Gas and LNG

Henry Hub held steady around $2.65 to $2.70/MMBtu through both sessions. AECO basis firmed on early Southwest US heat and subdued Gulf Coast LNG feedgas from seasonal maintenance. Globally, TTF and JKM both eased on US-Iran MOU progress, with JKM holding in the mid-$16s/MMBtu range and TTF retracing from its early-May Hormuz spike.

The story is Pakistan. State-owned Pakistan LNG Limited issued an emergency tender on May 6 for two spot cargoes (May 12 to 14 and May 24 to 26 delivery), the country's first spot purchase in nearly three years. Qatar and the UAE supply roughly 99% of Pakistan's LNG, all of it stuck behind Hormuz. Pakistan was actually reselling surplus cargoes as recently as January before the Qatar force majeure flipped it into shortage almost overnight. That is the cleanest single-country case for why LNG concentration risk is the structural trade of the decade, and a reminder that Asian physical demand has not gone away even as paper prices ease on diplomatic headlines.

Gold and the World Gold Council Release

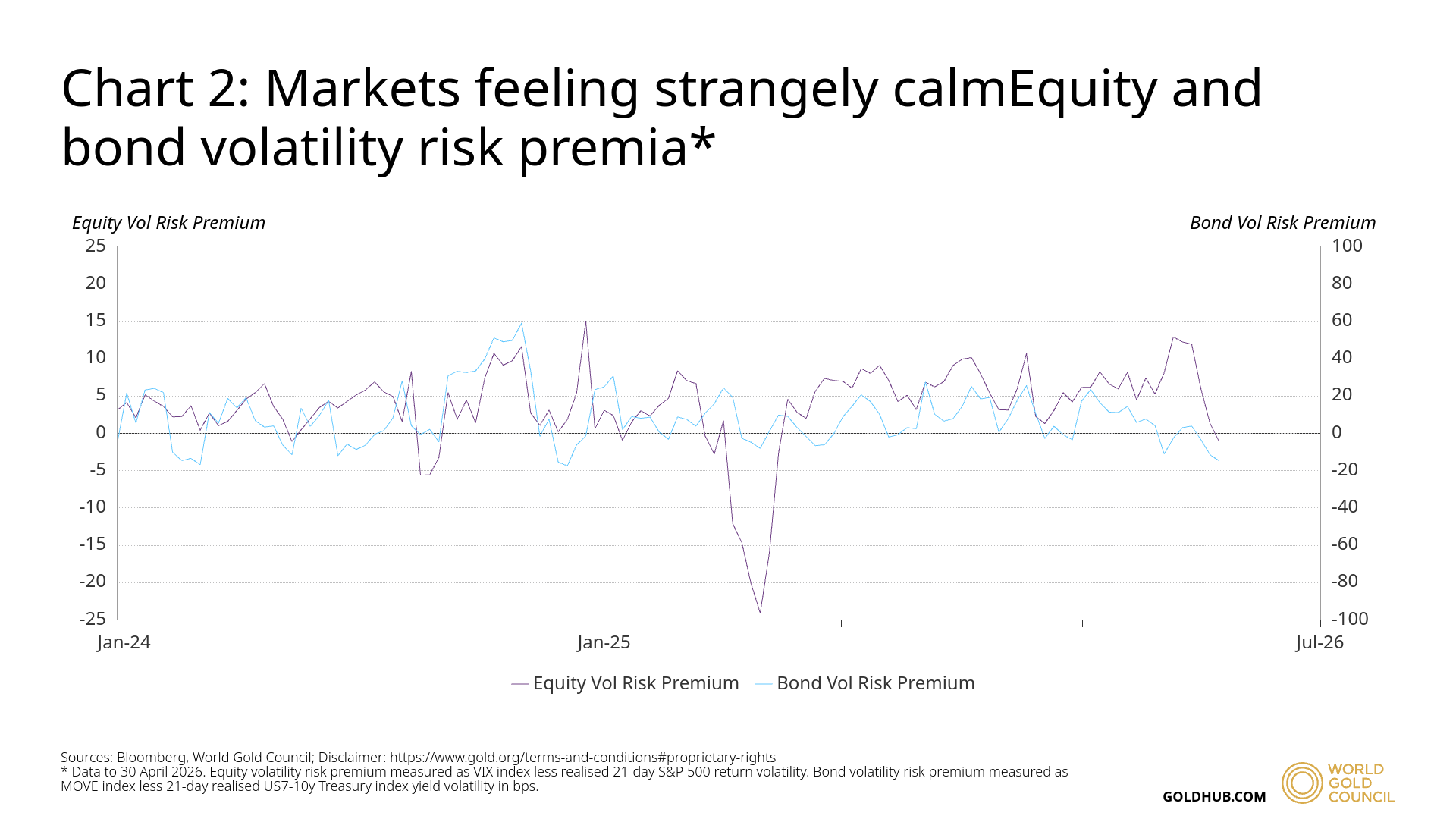

The gold market is currently navigating a period of high volatility, with spot prices retreating to $4,637 (May 7) from a May 6 close of $4,712. The current market is defined by a "strange calm" (Chart 2) that masks deep structural risks. While gold prices are technically soft, the underlying energy crisis is creating a stagflationary trap.

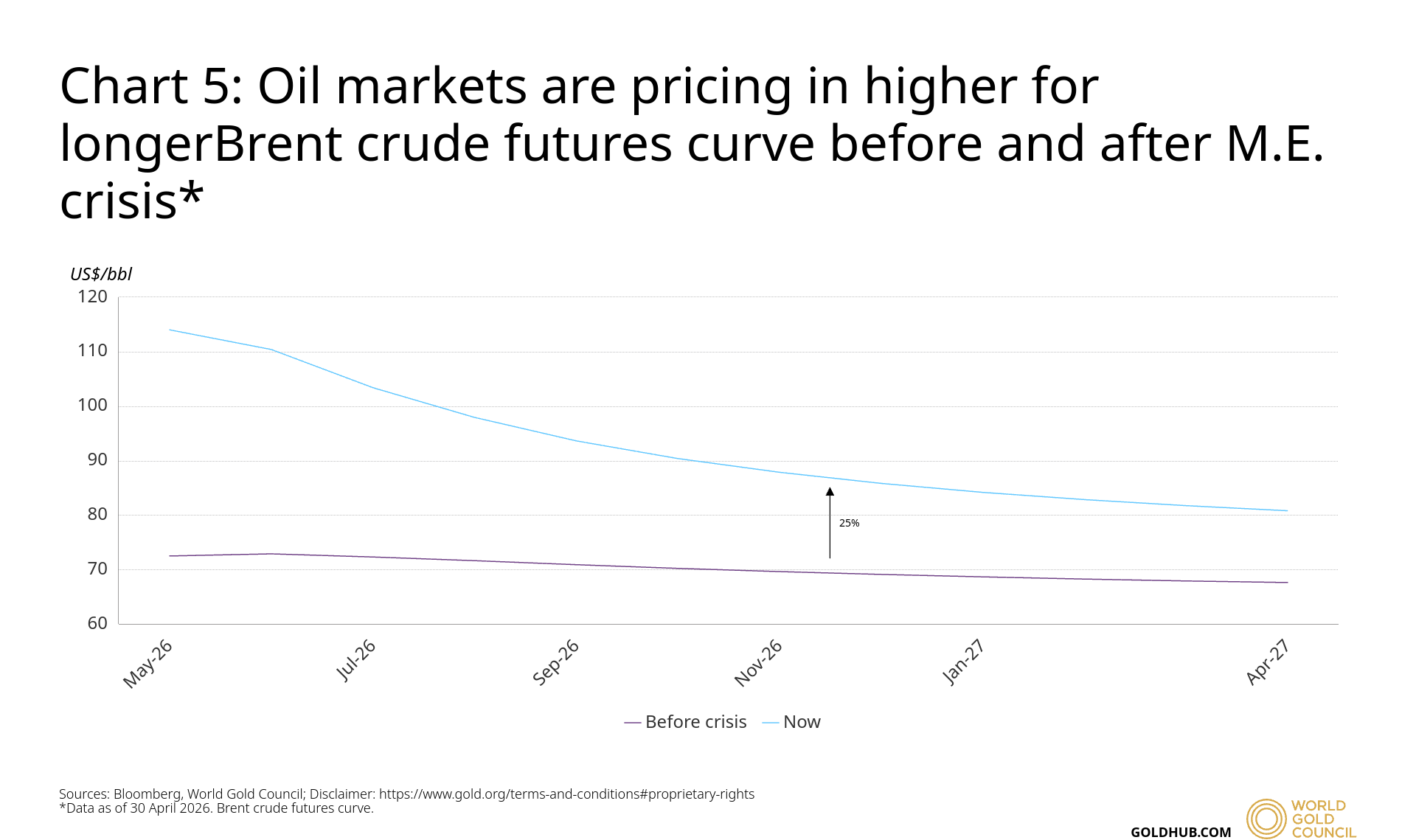

The Energy Problem: A Permanent ShiftAs shown in Chart 5, the market has priced in a 22–25% premium for Brent crude through 2027. This isn't a temporary spike; it’s a "higher-for-longer" reality.

The Crisis: With global oil inventories projected to hit an operational floor by September, the risk of disorderly pricing and severe demand destruction is high.

The Impact: These energy costs fuel inflation, forcing the Fed to remain hawkish, which currently weighs on gold’s price.

Gold: From Safe Haven to Liquidity SourceGold demand hit a record $193 billion in Q1, but the price is struggling.

The Divergence: Massive retail buying in Asia is being offset by US ETF outflows and technical selling.

The Liquidity Trap: In periods of high stress, gold is being sold to cover losses in other assets. If the "leveraged Treasury basis trade" unwinds, gold could see further liquidation before it recovers its safe-haven status.

The Problem with DiversificationChart 2 reveals a dangerous complacency. Equity and bond volatility premia have eased, suggesting markets feel the oil shock is containable.

The Reality: This "calm" is fragile. If the energy-led inflation becomes permanent, the current earnings cushion in US equities will evaporate.

The Solution: True diversification remains elusive; with gold futures positioning currently neutral, there is "dry powder" available for a massive rebound once the market realizes this stagflation is not temporary.

Markets are ignoring the 25% oil premium at their own peril. Gold is currently "soft" because it’s being used as a piggy bank, but it remains the primary hedge for the systemic deleveraging event that looms if oil supplies aren't restored.

Iran: State of Play

The market is pricing in a deal that is not yet signed.

The proposal: A one-page, 14-point MOU being negotiated by Witkoff and Kushner on the US side and Iranian officials via Pakistani mediators. It declares the war over and opens a 30-day window to negotiate the full agreement. Hormuz restrictions and the US blockade lift gradually during that window. The hard contingencies are pushed to phase two: Iranian moratorium on enrichment, US sanctions relief, release of frozen Iranian assets.

What moved this week:

Trump paused Project Freedom, the vessel escort operation

Naval blockade on Iranian ports stays in place

Iran's Revolutionary Guard said safe transit will be facilitated under new procedures, no specifics

France's Charles de Gaulle carrier group is moving toward the Red Sea as a backstop

Around 1,600 vessels and 23,000 seafarers remain stranded

Canadian Snapshot

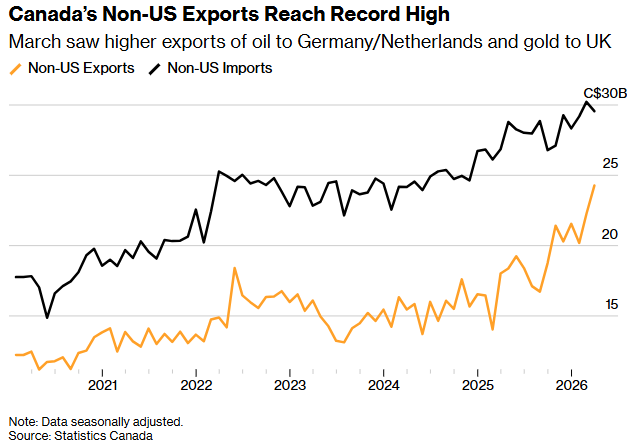

The headline this week is the trade data. StatsCan reported Tuesday that Canada swung to a C$1.8B trade surplus in March from a C$5.1B deficit in February, the first surplus in six months and a massive beat versus the C$2.5B deficit consensus. Two commodities did almost all the work:

Energy exports rose 15.6% to C$17.1B, the highest level since September 2022. The value of crude oil exports specifically jumped 18.9%, driven almost entirely by price (Hormuz closure), not volume.

Unwrought gold, silver, and PGM exports rose C$3B (+37.7%). The metal and non-metallic minerals export category overall hit a record high, up 24%.

Strip out energy and metals, and exports were up just 1.1% in value and down 0.3% in volume. The surplus is a war windfall, not broad-based external demand.

TSX Composite

Closed May 6 around 33,963 (+1.2%) after May 5's pullback to 33,567. Energy weighed despite earnings beats from Suncor and Cenovus (Cenovus posted an 83% profit jump on the MEG acquisition contribution), as falling oil overwhelmed the operational results. Banks led with RBC and TD up around 1% to 1.5%. Miners were the standout: Agnico Eagle and Barrick both up roughly 5%, Wheaton near 6%.

US Snapshot

S&P 500: 7,365.12 (+1.46%), record close. Nasdaq: 25,838.94 (+2.02%), record close. Dow: 49,910.59 (+1.24%). The risk-on bid on Iran de-escalation hopes was clean and broad, with 20 of 30 Dow names higher.

Sector tape: Energy down over 4% as expected on the oil collapse. Utilities off about 1.4%. Tech and consumer discretionary led, with Disney up 6.2% and Nvidia up 4.8%. AMD jumped post-earnings on AI strength.

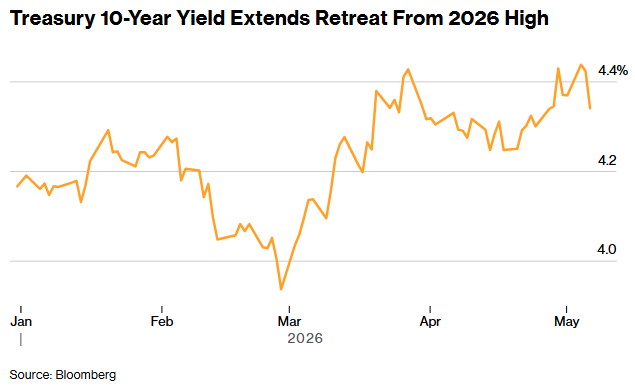

De-escalation Premium: Global bond yields are retreating as the 'One-Page' US-Iran peace proposal triggers a 10% collapse in Brent crude, effectively cooling the energy-driven inflation spike that has constrained central banks since February.

Watch list for Friday: April Nonfarm Payrolls and unemployment release, plus University of Michigan May inflation expectations. Any soft print on inflation expectations gives the Fed cover to acknowledge the energy spike is transitory, which is exactly the setup gold and rate-sensitive equities need.