Internal Market Brief

Friday May 8, 2026

Heavy week for crude. Three drivers: Project Freedom launching, US-Iran talks gaining traction, OPEC+ lifting June quotas. Crude sold off hard. Gas drifted sideways despite a bullish storage print. The real story sits in Canadian basis — spot diffs are dislocating well off bidweek indexes, which is real money for any producer pricing daily.

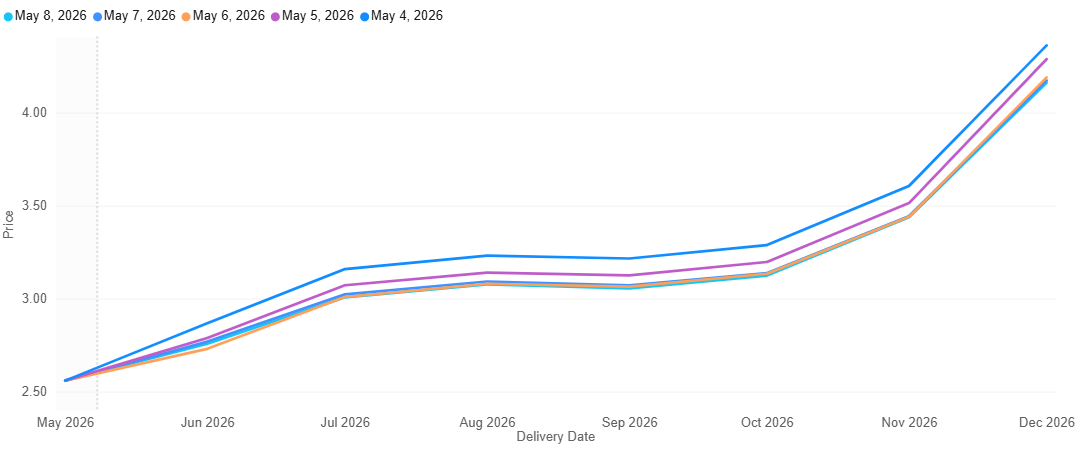

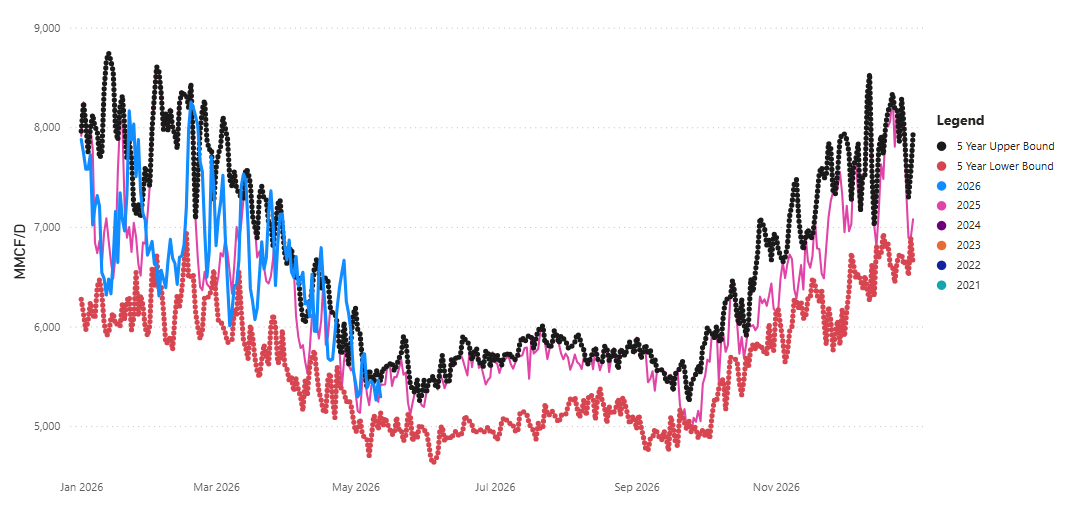

WTI

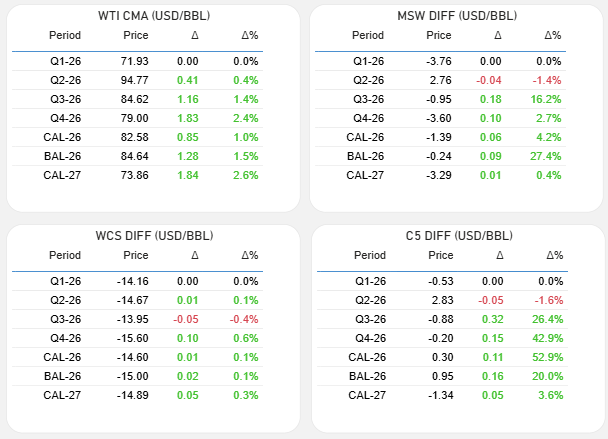

WTI CMA Bal-26

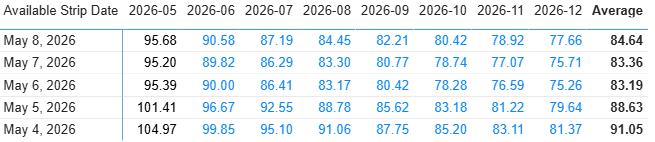

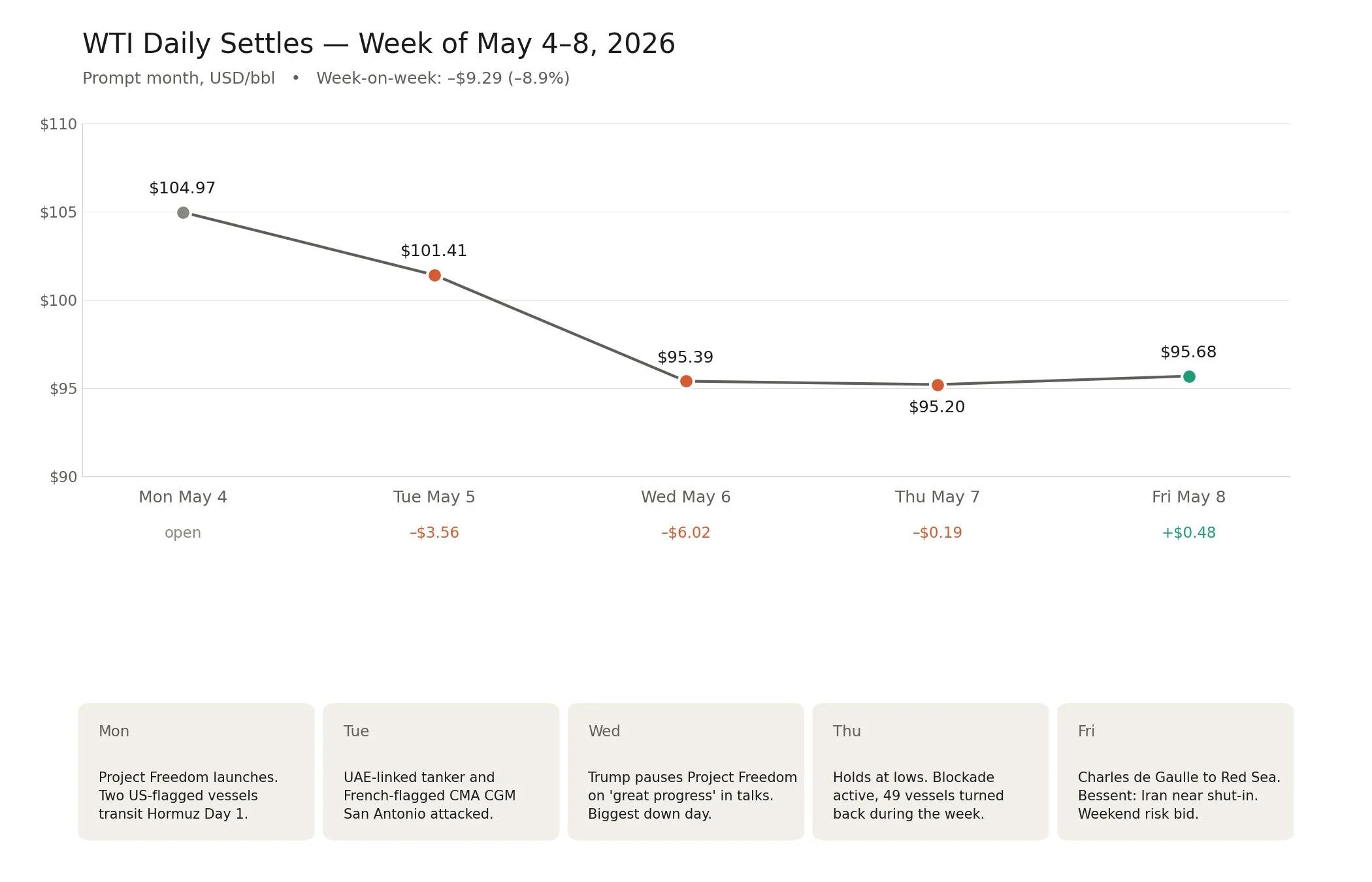

Prompt opened Monday at $104.97/bbl, bottomed Wednesday at $95.39/bbl after Trump paused Project Freedom, closed Friday at $95.68/bbl as weekend escalation risk re-entered. Week-on-week: prompt –$9.30/bbl, Bal-26 strip avg –$6.41/bbl.

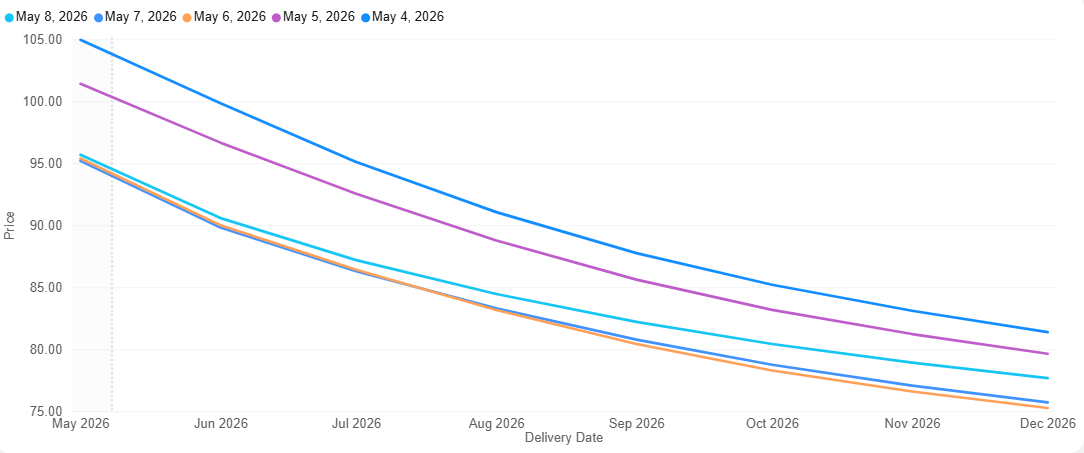

On the curve. Backwardation flattened but stayed steep because front and back are pricing different scenarios. Front holds residual Hormuz risk premium and reflects current Iranian shut-ins. Back is pricing post-deal normalization plus demand destruction from the recent $100+ prints. The curve doesn't flatten further until the deal is actually signed.

WTI Forecast Graph

OPEC+ raises June by 188 kbd, ignores UAE exit. Seven members lifted June quotas Sunday in the first meeting after UAE's April 28 withdrawal. The 188 kbd is rounding error against the ~14 mmbbl/d of Gulf flows still trapped behind Hormuz — messaging, not supply.

UAE's exit from OPEC is structurally bearish for crude. Under quota, UAE was producing 3.0 to 3.4 mmbbl/d, around 7 to 8 percent of OPEC+ output. Unconstrained nameplate is closer to 4 mmbbl/d, which means an incremental 0.5 to 1.0 mmbbl/d of supply once Hormuz reopens and those barrels can move. UAE Murban is light sour and competes directly with Iranian Light into the same Asian refining complex, so a post-deal world has both producers chasing the same Chinese and Indian buyers. The signaling risk compounds it: if UAE can walk when quotas no longer suit it, Iraq and Kazakhstan have less reason to comply with theirs. None of this prices into the front of the curve today with Hormuz still closed, but it is the structural reason deferred contracts have lagged the war premium unwind.

US fundamentals stayed tight against the tape. EIA commercial crude –2.3 mmbbl to 457.2 mmbbl, SPR –5.2 mmbbl to 392.7 mmbbl. Refinery utilization 90.1%, crude inputs 16.0 mmbbl/d. Bullish prints, bearish price — market is trading geopolitics over fundamentals.

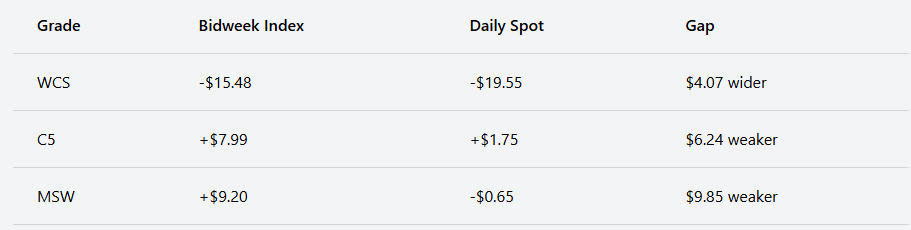

Canadian Differentials

Spot vs bidweek index is the story. Producers pricing daily underperformed materially in May:

MSW: spot –$0.65 vs index +$9.20 = $9.85 gap

C5 BLX4: spot +$1.75 vs index +$7.99 = $6.24 gap

WCS: spot –$19.55 vs index –$15.48 = $4.07 widening

WCS at Hardisty is now at its widest since the war began. Trans Mountain running full means egress is the binding constraint.

Grade moves vs WTI prompt (–$9.30). Lights and condensates moved roughly with WTI on flat price, but the Hormuz light premium unwind was a separate negative on top. Heavies got hit twice — WTI selling off, plus the WCS diff widening another ~$4. So WCS flat-price fell closer to $13 against WTI's $9.30. Producers running daily on lights got hammered on the spot/index gap; heavy producers got hammered on the diff.

Split reflects the structural drivers — light/sour premiums are Hormuz-driven and unwind on supply normalization. WCS is egress-constrained regardless of global flows.

June opens weaker. Lights +$2.50 on MSW, condensates +$2.82 on C5, WCS –$15.91. Spot and index roughly flat to each other for June — no dislocation yet. Heavy netbacks under pressure on June WTI CMA of $90.58/bbl.

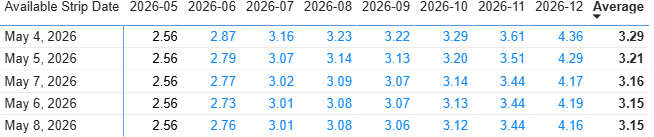

NYMEX NG

NYMEX NG Forecast Graph

NYMEX NG Bal-26

June contract fell $2.87 → $2.76/MMBtu. Bal-26 strip avg $3.29 → $3.15/MMBtu (–$0.14), with the back falling most in absolute terms — Dec-26 –$0.20. Wednesday's selloff tracked the broader risk-off on US-Iran headlines.

Bullish print, bearish tape. EIA reported 63 Bcf injection vs 74 Bcf consensus and 77 Bcf 5-year avg. Inventories at 2,205 Bcf, surplus to 5-yr narrowed to 139 Bcf from 153 Bcf. Futures rallied 4 cents on the print, gave it all back by Friday.

Production supportive, LNG capped. Lower 48 dry gas at one-week lows of 109.7 Bcf/d as EQT and others curtail. Offsetting: LNG feedgas easing from April record on Gulf Coast spring maintenance. JKM and TTF still above $15/MMBtu — US export capacity at max utilization, no arb until new liquefaction lands.

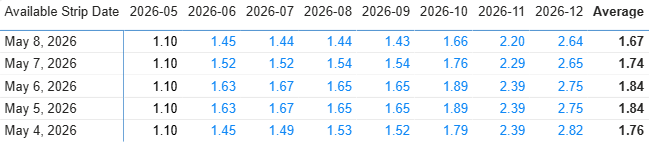

AECO 7A

Daily 7A opened and closed at $1.10/GJ on the May index. June-26 spiked $1.45 → $1.63/GJ Monday-Wednesday on residual cold demand and short covering, then collapsed back to $1.45/GJ by Friday. Back of curve got hit harder — Dec-26 $2.82 → $2.64, Bal-26 strip avg $1.76 → $1.67/GJ.

Intraprovincial Storage Graph

Storage in range, demand softening. Alberta intraprovincial storage near 5-year avg, no capacity pressure. Field receipts from Groundbirch steady into NGTL; West Gate deliveries holding ~2 Bcf/d. Near-term weather supports injections.

LNG Canada the structural pull. Kitimat delivered its 80th cargo with both trains operational. Marine terminal expansion underway. Phase 2 FID expected year-end 2026 under Building Canada Act fast-track — would double Kitimat from 14 to 28 mtpa.

AESO power in contango. May pool $28.43/MWh vs June forward $38.00/MWh — $9.57 step-up on summer cooling and data center load.

Iran: State of Play

The market is pricing in a deal that is not yet signed.

The proposal: one-page, 14-point MOU between Witkoff/Kushner and Iranian officials via Pakistani mediators. Declares the war over, opens a 30-day window for the full agreement. Hormuz restrictions and naval blockade lift gradually; hard contingencies (enrichment moratorium, sanctions relief, frozen asset release) pushed to phase two.

What moved this week:

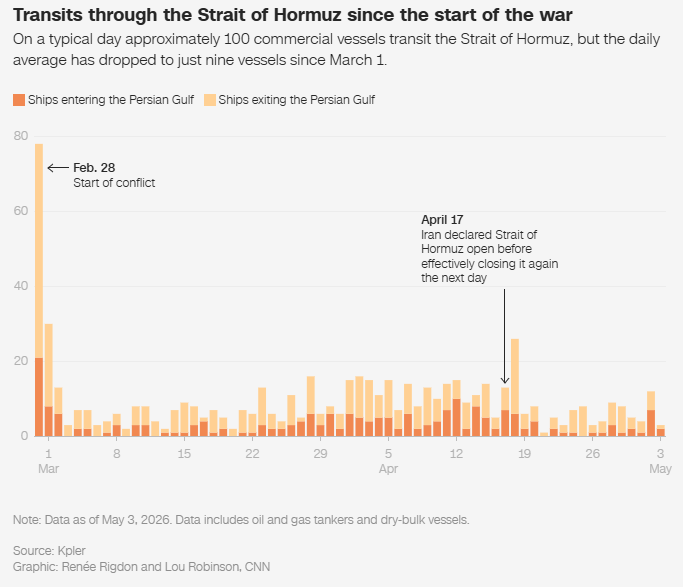

May 4: Trump launched Operation Project Freedom, a U.S. Navy mission to escort merchant vessels through the Strait of Hormuz. Two U.S.-flagged ships completed transit on Day 1.

May 6: Trump paused Project Freedom citing "great progress" in negotiations. The naval blockade on Iranian ports remained active, with CENTCOM reporting 49 commercial vessels turned back during the week.

Mid-week: A UAE-linked tanker and the French-flagged CMA CGM San Antonio container vessel were attacked during transit attempts, crew evacuated for medical care.

Late week: France's Charles de Gaulle carrier group repositioned toward the Red Sea as backstop force. Approximately 1,550 commercial vessels and 22,500 mariners remain stranded in or around the strait. Carra Globe

Treasury comment: Secretary Bessent indicated Iran may need to begin shutting in production within weeks as both floating and onshore storage capacity approach saturation, with the blockade having deprived Tehran of meaningful oil revenue.

Weekend May 10: Trump rejected Iran's latest response, sending Brent up 3.5% intraday and re-injecting weekend risk premium back into the front of the WTI curve.

Hormuz flows still at ~5% of pre-war. Kpler shows 191 vessel transits in all of April vs pre-war monthly avg near 3,000. Of the limited flows resuming: NITC dark-fleet vessels are running ship-to-ship transfers off Malaysia and landing in Shandong teapot refiners and Indian private refiners (Reliance, Nayara). Gulf-flagged tankers (Saudi, Kuwait, Iraq) are the ones the USN was escorting under Project Freedom — those flows paused with the mission. Friendly flag-state escort arrangements being negotiated.

Insurance markets pricing residual risk at ~20x pre-war (5% of hull value vs 0.25%). DHL guiding 4-6 months to normalize. Market is trading the probability of a deal more than the physical reality of flows.

Canadian Snapshot

March trade data (May 6): Canada flipped to a C$1.8B surplus, first in six months, beat vs –C$2.5B consensus. Energy exports +15.6% to C$17.1B, highest since Sept 2022. Crude exports +18.9% driven entirely by price, not volume — Hormuz windfall flowing directly into Calgary producer revenue. Ex-energy and metals, exports +1.1%.

April jobs (May 8): –18k vs +10k consensus. Unemployment 6.9%. TD now expects BoC on hold for the rest of 2026 if oil reverses. Keeps CAD pinned 1.36–1.38 — modest headwind for producer netbacks since barrels price in USD.

Equities: TSX closed Friday at 34,078 (+0.6%). Enbridge, Cardinal, Suncor, Cenovus all beat — Cenovus +83% on MEG contribution. Energy gave back gains as WTI sold off mid-week.

US Snapshot

Sixth straight weekly gain for US equities. Energy the only major sector down hard (–4%) as oil collapse overwhelmed strong major earnings.

10-year –3.4 bps Friday on Iran de-escalation bid. Setup is "lower oil, lower inflation, equity-friendly" — every step toward a deal trades as risk-on, crude-bearish. If the deal falls apart, the front of WTI has the most upside given how much war premium has been removed.

April NFP (May 8): +115k vs +65k consensus. Unemployment steady at 4.3%. Supports Fed-on-hold — softer dollar, lower real rates support oil-equity valuations.